Nobody sets out to buy a car with outstanding finance on it.

That would be plain daft.

However, a surprising number of used car buyers fall into this trap.

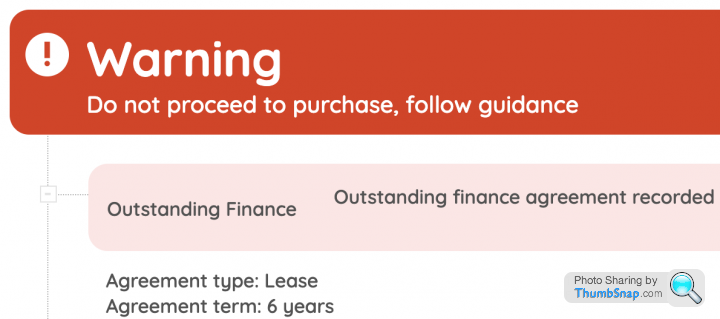

If you do buy a car on which money is still owed, you could lose the car and all the money you have paid for it. That’s the stark warning from the used car history check people at HPI and the Finance and Leasing Association (FLA).

HPI has found that one-on-four of the cars it checks are subject to an outstanding finance agreement. ‘Whether you are a first time buyer on a tight budget or someone looking to upgrade your current car, check the facts before you buy,’ says Nicola Johnson, Consumer Services Manager for HPI. ‘If you don’t you could face the car of your dreams being repossessed by the finance house that rightly owns it.’

Be wary of dealers who have not carried out a history check on their stock.

If they haven’t, make sure you do.

It’s also worth remembering that not all history checks go into the same depth.

Make sure any check you pay for will alert you if the car has been stolen, written off or still has money owed on it.